This article breaks down why early investing matters more than a high income, explains the magic of compounding in simple terms, and highlights the best beginner-friendly investment options like SIPs, NPS, ELSS, PPF, and direct stocks.

Most people believe that investing is for the wealthy—something to think about only when you have extra cash lying around. But the real secret to retiring rich isn’t earning a massive salary or hitting a jackpot. It’s starting early, even if you’re broke.

If you’re earning just enough to cover your expenses, investing might seem impossible. But what if you could turn even ₹500 a month into lakhs, or even crores, over time? Thanks to compounding, strategic tax-saving investments, and the right financial habits, wealth isn’t about how much you start with—it’s about how long you stay invested.

Investing is for the rich. I’ll start when I have extra money.

Let’s consider two people:

Even though Rahul invests twice as much, Aditi will still retire wealthier. Why? Compounding. The extra years she stays invested amplify her returns exponentially.

This is why small, consistent investments in your 20s can outweigh larger investments made later in life.

Compounding refers to the process where your investment generates earnings not only on the original amount (the principal) but also on the interest accumulated over time - resulting in accelerated, exponential growth. Unlike simple interest, which is calculated solely on the principal, compound interest allows your money to grow faster the longer it remains invested.

How compounding works:

Let’s say you invest ₹5,000 per month in a mutual fund with an average annual return of 12%:

This is why investing early is more powerful than investing more later in life.

Even if you have just ₹500-₹1,000 per month, you can start building wealth. Here’s how:

1. Mutual Funds via SIPs (Start With ₹500)

2. National Pension System (NPS)

3. Equity-Linked Savings Scheme (ELSS)

4. Public Provident Fund (PPF)

5. Direct Stocks – High-Risk, High-Reward

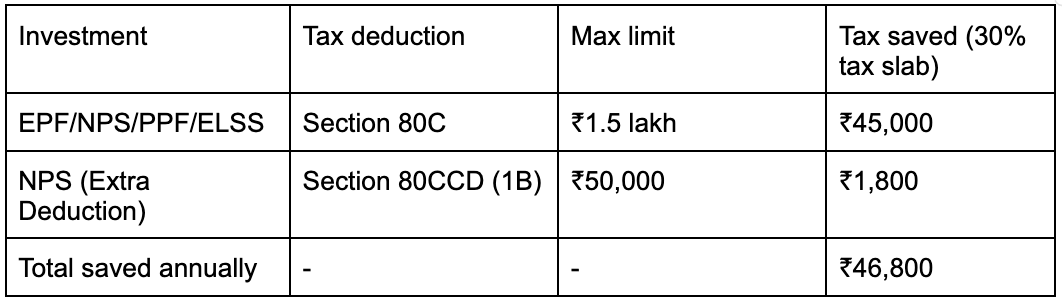

If you’re salaried, you can legally save up to ₹46,800 in taxes every year. Here’s how:

This means, if you invest smartly, the government literally gives you free money by reducing your tax liability.

The biggest mistake isn’t investing too little—it’s not investing at all. Even if you start with ₹500, the habit matters more than the amount. You don’t need a big paycheck to retire rich. What you need is consistency, patience, and time in the market.

So, if you’re broke today, don’t wait until you have ‘extra’ money to start investing. Start with whatever little you can—because time is your biggest financial asset.

This blog explains how to maximize rewards and savings using a RuPay credit card linked to UPI. It highlights the benefits of SalarySe UPI powered with Credit.

This article breaks down why early investing matters more than a high income, explains the magic of compounding in simple terms, and highlights the best beginner-friendly investment options like SIPs, NPS, ELSS, PPF, and direct stocks.

This Diwali, skip the EMI stress and shine smarter. With SalarySe and BytePe’s new iPhone 17 subscription, enjoy India’s most loved smartphone for just ₹3,700/month, stay worry-free with damage protection, and upgrade every year with ease. Because the brightest celebrations deserve the smartest choices.